The Middle East petrochemical supply chain disruption triggered by escalating tensions in the Gulf has sent shockwaves through the global chemical industry. For PVC manufacturers, compounders, and buyers worldwide, the consequences are immediate and measurable: raw material costs are rising, lead times are extending, and supply reliability is under serious threat. Understanding how Gulf conflict translates into real-world price pressure on PVC feedstocks is no longer optional — it is critical intelligence for every procurement and operations team in the polymer value chain.

This article examines the mechanics of how conflict in the Middle East disrupts ethylene, chlorine, and ethylene dichloride (EDC) supply flows, how the Strait of Hormuz crisis amplifies price risk, and what actionable steps chemical buyers can take to protect their operations.

Why the Gulf Region Is Central to Global PVC Feedstock Supply

The Middle East’s Role in Petrochemical Production

The Middle East accounts for roughly 17–20% of the world’s ethylene capacity and is a major exporter of ethylene dichloride (EDC), vinyl chloride monomer (VCM), and caustic soda — all core inputs for PVC production. Countries including Saudi Arabia, Iran, Kuwait, and the UAE operate some of the world’s most cost-competitive petrochemical complexes, supported by access to subsidized natural gas feedstocks.

When Gulf energy trade is stable, these facilities supply chemical manufacturers across Asia, Europe, and Africa at competitive prices. When conflict threatens infrastructure, shipping lanes, or insurance access, the entire global supply chain feels the pressure.

Iran’s Pivotal Position in Petrochemical Exports

Iran is the second-largest petrochemical producer in the Middle East, with an installed capacity exceeding 100 million tonnes per year across its various facilities. Despite operating under sanctions, Iran has continued to export polymers, methanol, and base chemicals — often through indirect channels to markets in Southeast Asia and China.

The impact of Iran conflict on petrochemical exports extends beyond Iran’s own production. Any escalation involving Iranian military assets in the Gulf creates immediate risk to the broader regional shipping environment, regardless of which facilities are directly affected.

The Strait of Hormuz: The World’s Most Critical Maritime Chokepoint

Strait of Hormuz crisis scenarios represent the single greatest supply risk in global energy and chemical trade. Approximately 20–21 million barrels of oil per day transit through the Strait — roughly 20% of total global petroleum liquids. More critically for the chemical industry, the Strait is also the primary corridor for:

- LNG exports from Qatar, the world’s largest LNG exporter

- Naphtha and ethane shipments that feed Asian and European crackers

- EDC and VCM cargoes from Gulf-based petrochemical plants

- Caustic soda and chlor-alkali products destined for PVC producers in Asia

Even a partial Strait of Hormuz closure — or the credible threat of one — is enough to trigger a sharp repricing of chemical feedstocks across forward markets. Insurance underwriters immediately revise war-risk premiums for oil tanker routes through the region, raising the landed cost of every cargo passing through Gulf shipping lanes.

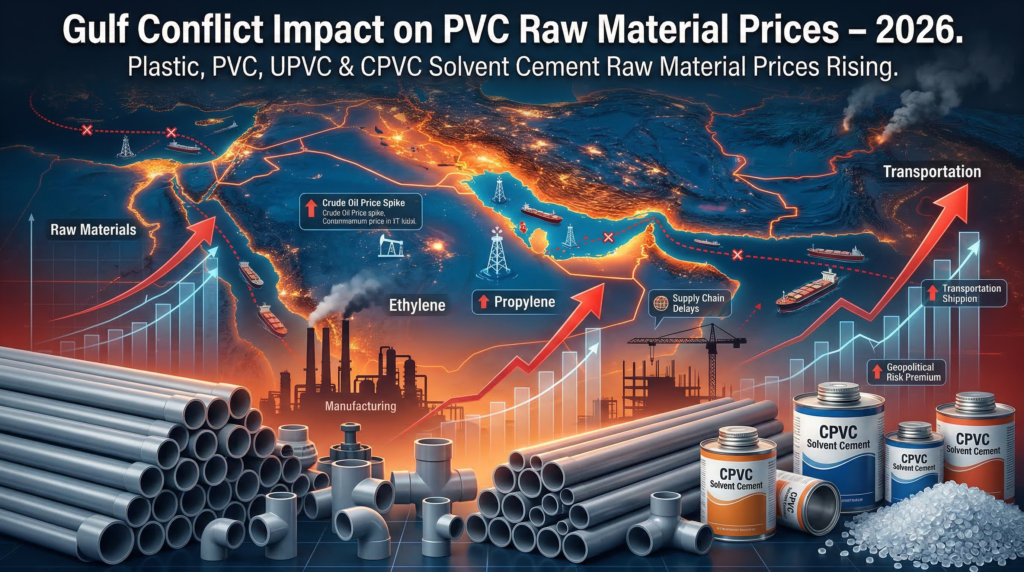

How Shipping Disruptions Translate Into PVC Price Increases

The cost transmission mechanism from Gulf conflict to PVC prices works through several reinforcing channels:

| Disruption Channel | Impact on PVC Raw Material Costs |

| Crude Oil Price Spike | Naphtha and ethane costs rise, increasing ethylene production costs globally |

| Freight Rate Surge | Tanker charter rates double or triple within days of conflict escalation |

| War-Risk Insurance Premium | Adds $3–8/tonne to cargo costs for Gulf-origin shipments |

| Port Congestion & Delays | Buyers front-load inventory, causing spot price spikes and hoarding |

| LNG Export Disruption | Raises energy costs for European and Asian chlor-alkali producers |

Disruption of Petrochemical Feedstock Shipments: The PVC-Specific Impact

Ethylene and EDC Supply Tightening

PVC is produced via two primary routes — the ethylene-based process (using EDC and VCM) and the carbide process. The ethylene-based route dominates globally and is directly exposed to disruption of petrochemical feedstock shipments from the Middle East. When Gulf crackers reduce output or when tankers cannot safely transit key oil shipping routes, EDC availability tightens globally within weeks.

During the 2019 Gulf of Oman tanker attacks, EDC spot prices in Asia rose by approximately 8–12% within 30 days. During the Red Sea disruption of late 2023, shipping costs from the Middle East to Asia rose by 200–300% for certain routes, with direct knock-on effects for specialty chemical and polymer trade.

Chlorine and Caustic Soda: The Hidden Vulnerability

Chlorine is produced via electrolysis of brine and is co-produced with caustic soda. While chlorine itself is rarely shipped internationally due to its hazardous nature, its precursor — caustic soda — is traded globally in significant volumes from Gulf-based chlor-alkali plants.

Energy trade disruption that raises electricity and gas costs for chlor-alkali producers translates directly into higher chlorine equivalent costs for PVC manufacturers. A 10% rise in energy costs for a chlor-alkali plant typically increases production costs by $15–25 per tonne of EDC equivalent — a meaningful margin in a commodity market.

Global Chemical Industry Impact: Broader Ripple Effects

The global chemical industry impact from Strait of Hormuz closure extends well beyond PVC. Polypropylene, polyethylene, methanol, ammonia, and styrene supply chains are all exposed to Gulf feedstock risks. However, PVC is particularly vulnerable for several reasons:

- High dependence on chlorine, which has limited geographic diversification in supply

- Concentrated production in China, which relies on imports of EDC and VCM from the Gulf

- Limited ability to substitute materials in core applications like pipes, cables, and flooring

- Relatively thin producer margins that amplify the impact of feedstock cost increases

Price Volatility: Historical Data Points

Historical conflict events provide clear precedents for the price impact of Gulf tensions:

- 2019–2020 Gulf tensions (post-Aramco attack): Naphtha prices spiked 15% in two weeks; PVC prices in Asia rose 5–8% over the following month.

- 2022–2023 Russia-Ukraine War (secondary effect): Rerouted energy flows tightened European naphtha supply, raising EU PVC production costs by an estimated €40–60/tonne.

- 2023–2024 Red Sea Crisis: Container shipping rates from Asia to Europe tripled; specialty chemical delivery windows extended by 3–5 weeks on average.

In each case, the immediate price response overshot the underlying supply disruption, as buyers moved to secure inventory ahead of anticipated shortages.

Pros, Cons, and Key Market Insights for PVC Buyers

Who Benefits From Gulf Supply Disruption

Not all market participants suffer equally from Middle East oil supply shocks. Some players are structurally advantaged:

- North American PVC producers using shale-derived ethane face lower feedstock cost exposure and gain relative competitiveness during Gulf crises.

- Integrated producers with captive chlorine capacity are shielded from external caustic soda price swings.

- Traders holding physical inventory in Europe or Asia can realize significant windfall gains during short-term supply squeezes.

Who Bears the Greatest Risk

- Spot buyers without long-term contracts face the full brunt of oil price volatility.

- Converters in South Asia and Southeast Asia, heavily dependent on Gulf-origin EDC and VCM, face both higher prices and extended lead times simultaneously.

- Small-to-mid-size PVC processors with limited working capital cannot absorb large inventory builds without financial strain.

Expert Strategies: How Chemical Buyers Can Respond

Experienced procurement teams treat geopolitical risk as a permanent feature of their operating environment, not an exceptional event. Here are the proven strategies for managing Gulf conflict exposure in PVC and polymer supply chains:

1. Diversify Supply Origins

Reduce reliance on Gulf-origin EDC and VCM by qualifying suppliers in the US (ethane-based), Taiwan, and India. Dual-sourcing from at least two geographic regions provides meaningful protection against regional disruptions.

2. Build Strategic Buffer Inventory

For PVC resin and key additives, maintain a minimum 30–45 day forward inventory buffer during periods of elevated Gulf tension. This cost must be weighed against the operational risk of a supply gap during a conflict escalation.

3. Use Price Review Clauses in Contracts

Negotiate force majeure and price adjustment clauses in long-term supply agreements that specifically reference geopolitical disruptions to oil tanker routes and global oil markets. This transfers some price risk back to suppliers with more diversified supply bases.

4. Monitor Leading Indicators

Track these early-warning signals for PVC feedstock disruption risk:

- Strait of Hormuz shipping insurance premiums (available via Lloyd’s of London market reports)

- Brent crude oil futures spread (contango steepening signals hoarding behavior)

- EDC and VCM spot price indices published by ICIS and Platts

- LNG spot price premiums in Asia vs. TTF (European benchmark)

- Freight rate indices for Middle East-to-Asia tanker routes (Baltic Exchange)

5. Engage a Chemical Trade Specialist

Consider retaining a specialist chemical trading advisory firm with real-time visibility into Gulf energy trade and petrochemical cargo movements. The cost of this intelligence is typically recovered many times over in a single procurement cycle during a market disruption event.

Real-World Example: The 2023 Red Sea Crisis and PVC Markets

The Houthi attacks on commercial shipping in the Red Sea beginning in November 2023 provide a recent and highly instructive case study. Within six weeks of the first attacks:

- Container freight rates from Asia to Northern Europe rose from approximately $1,500/FEU to over $6,000/FEU.

- Ships rerouting around the Cape of Good Hope added 10–14 days to delivery schedules.

- Several major chemical distributors in Europe issued force majeure notices for shipments originating in Asia and the Middle East.

- PVC compound prices in Germany and the UK rose by 4–7% between December 2023 and February 2024, driven by supply uncertainty rather than actual shortage.

The critical insight from this episode: price impact from Gulf conflict is as much psychological as physical. Buyers react to perceived risk, often before actual supply is interrupted, creating self-reinforcing price spirals. Companies that maintained disciplined inventory levels and had pre-qualified alternative suppliers were able to resist spot market pressure and wait for normalization.

Conclusion: Proactive Risk Management Is the Only Viable Strategy

The Middle East petrochemical supply chain disruption driven by Gulf conflict is not a temporary anomaly — it is a structural feature of the global chemical market for the foreseeable future. From the potential closure of the Strait of Hormuz to the ongoing Iran conflict and its effects on petrochemical exports, every escalation in Gulf tensions carries measurable consequences for PVC raw material prices, global oil markets, and chemical trade flows.

PVC buyers, manufacturers, and traders who treat geopolitical risk as an integral part of their procurement and supply chain strategy will consistently outperform those who react only after disruption occurs. The tools are available: supply diversification, strategic inventory, intelligent contract structures, and real-time market intelligence. The question is not whether the next Gulf crisis will affect your supply chain — it is whether you will be prepared when it does.

Organizations that build geopolitical resilience into their operations today are the ones that will maintain continuity, protect margins, and gain competitive advantage when the next disruption of petrochemical feedstock shipments from the Middle East arrives.

Frequently Asked Questions (FAQ)

Q1: How does Gulf conflict directly affect PVC raw material prices?

Gulf conflict raises PVC raw material prices through multiple mechanisms: crude oil price spikes increase naphtha and ethane costs for ethylene production; Strait of Hormuz disruptions restrict the flow of EDC, VCM, and caustic soda from Middle East producers; and war-risk insurance premiums add $3–8 per tonne to cargo costs. The combined effect can increase PVC resin prices by 5–15% within 4–8 weeks of a major escalation event.

Q2: What percentage of global PVC feedstock comes from the Middle East?

The Middle East supplies approximately 15–20% of global ethylene capacity and is a significant exporter of EDC and VCM, particularly to Asia. Iran alone accounts for a meaningful share of global methanol and polymer exports. Any major disruption to Gulf energy trade therefore has global repercussions for PVC feedstock availability and pricing.

Q3: What happens to PVC prices if the Strait of Hormuz is closed?

A full closure of the Strait of Hormuz would be catastrophic for global chemical markets. LNG exports from Qatar — which supply energy for chlor-alkali and cracker operations across Asia and Europe — would be immediately halted. Oil prices would spike by an estimated $20–40 per barrel within days, driving naphtha and ethane costs sharply higher. PVC prices could rise by 20–40% within 60 days, depending on the duration of the closure and the availability of alternative supply routes.

Q4: Which PVC-producing regions are most exposed to Middle East supply disruption?

South and Southeast Asia bear the greatest exposure, as these regions are heavily dependent on imports of EDC and VCM from Gulf-based petrochemical facilities. China, while the world’s largest PVC producer, also relies on imported feedstocks and is exposed to shipping route disruptions. European manufacturers face secondary exposure through LNG pricing and naphtha supply tightness.

Q5: What are the best strategies for PVC buyers to protect against Gulf conflict supply risk?

The most effective strategies include: (1) geographic diversification of EDC and VCM suppliers to include non-Gulf sources; (2) maintaining 30–45 days of strategic buffer inventory during elevated geopolitical risk periods; (3) negotiating price review and force majeure clauses in supply contracts; (4) monitoring leading indicators such as Brent crude spreads, Baltic Exchange tanker rates, and ICIS spot price indices; and (5) engaging specialist chemical trade intelligence services for real-time market visibility.